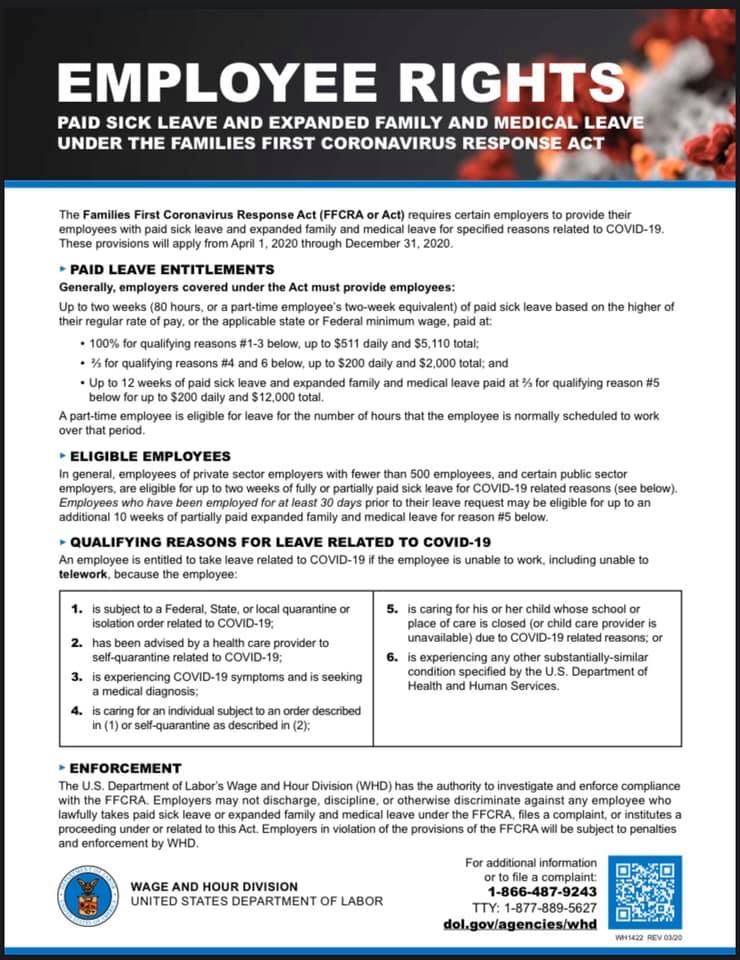

It will likely be a long time before we fully…

1099 independent contractors and CARES Act forgivable loans

Several people have asked how the Paycheck Protection Program forgivable loans (sometimes referred to as grants) created by the CARES Act apply to 1099 independent contractors. The early information released by the Small Business Administration created a lot of confusion on this topic. On April 2, the SBA released new regulations that clarified it.

Let’s use an example to help make it clear. Let’s say a company called XYZ Enterprises, Inc. has 10 employees and an owner who works at the company. XYZ Enterprises also uses the contract services of Bob Smith, and issues him a 1099 each year.

Here’s how the PPP loans would work in this situation:

- XYZ Enterprises can apply for a PPP forgivable loan. When calculating the amount of the loan, they will use 2.5x their average payroll expenses for their 10 employees and the owner who works and receives a salary. (Note that salaries are capped at $100,000.00 for the calculations.)

- XYZ Enterprises is NOT allowed to include Bob Smith’s payments in their calculations.

- When XYZ Enterprises gets their loan, they are to use it for payroll expenses (to keep people employed and at their ordinary wages and salaries), as well as for utilities, rent for a pre-existent lease, and interest on pre-existent mortgages. All monies from the loan spent on these in the first 8 weeks after the loan is given will be forgiven. If they spend the money on Bob Smith, the amounts paid to him will NOT be forgiven because Bob is not an employee. He is his own separate business “entity.” But that does not mean that Bob is out of the discussion.

- Bob, as an independent contractor, has the ability to file for his own PPP forgivable loan. He is seen as a separate business – NOT an employee of XYZ Enterprises.

What is still unclear is when Bob can apply. The Treasury Department has stated that small businesses and “sole proprietors” can apply starting 4/3. They state that “independent contractors” and “self-employed individuals” can begin applying on 4/10. In the law, sole proprietors, independent contractors, and self-employed are often overlapping terms. The regulations to this point are silent on the issue. Our current educated guess is that “sole proprietor” is referring to people who have a limited liability company that has elected “sole proprietor” tax status. However, it is still unclear and we are seeking opinions.

For now, we are suggesting anyone who wants to seek a PPP forgivable loan start the process immediately. If your bank does not believe you meet the definition of “sole proprietor,” you will be postponed to 4/10. We will try to provide more information as regulations are updated.

Contact us if you have other questions about this process.

Related Posts